As we enter the 2026 real estate season, Denver homebuyers are navigating a new era of taxation. The passage of the “One Big Beautiful Bill” Act (OBBBA) in July 2025 has officially replaced many expiring TCJA provisions, bringing much-needed clarity to the tax benefits of buying a house.

Whether you are eyeing a bungalow in Wash Park or exploring Denver luxury real estate, understanding these 2026 updates is essential for your financial planning.

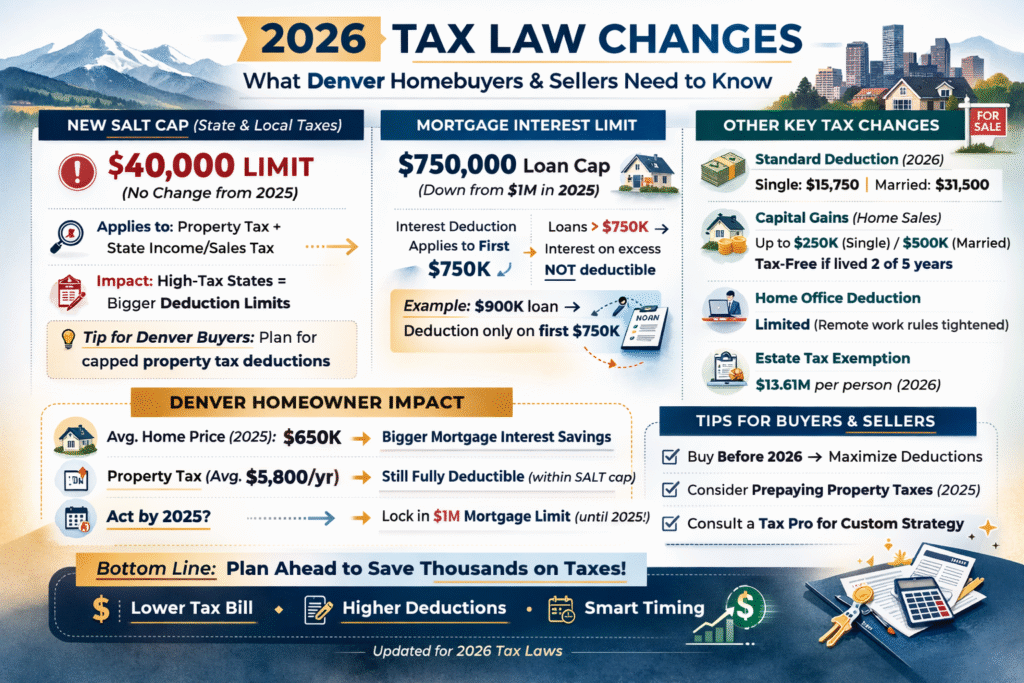

The Mortgage Interest Deduction in 2026: The $750,000 Cap Remains

Despite the sunset of older laws, the mortgage interest deduction 2026 rules under the OBBBA have maintained the cap on deductible mortgage debt at $750,000 for new home purchases.

- Primary and Second Homes: You can still deduct interest on a combined debt of up to $750,000 across two homes.

- Grandfathered Mortgages: If you bought your home before December 2017, you may still be eligible for the older $1 million limit.

In a high-value market like the Mile High City, this cap means that many Denver homebuyers will need to carefully calculate their “after-tax” monthly payment before making an offer.

Planning a Move in 2026?

Navigate the Denver market with confidence. Our latest guide covers everything from neighborhood trends to the 2026 closing process.

The SALT Deduction Update: Good News for Colorado Homeowners

One of the biggest wins in the 2026 tax code is the adjustment to the SALT deduction limit. Under the OBBBA, the previous $10,000 cap on State and Local Taxes has been increased to $40,000 for both single and joint filers.

For residents in high-value Denver metro counties, this shift allows you to deduct a significantly larger portion of your state income tax and Colorado property taxes, making homeownership more affordable than it has been in years.

2026 Denver Property Tax Relief and Credits

At the state level, Colorado has introduced additional measures to combat rising assessments. Under recent legislation (including updates from HB24B-1004), many homeowners are eligible for:

- Property Tax Deferral Programs: Now expanded for 2026 to assist seniors and active military members.

- Wildfire Mitigation Credits: Available for homeowners in specific Colorado zones who invest in “defensible space” improvements.

Home Equity Loans: Is the Interest Still Deductible?

The OBBBA clarifies that home equity loan interest is tax-deductible only when the funds are used to “substantially improve” the dwelling. If you are taking out a loan to renovate a kitchen in a Hilltop classic or add a suite to a Highlands duplex, the interest remains a powerful tax write-off.