Navigating the rising average cost of college in Colorado in 2026 requires a proactive strategy. For parents looking at institutions like CU-Boulder, where the estimated in-state cost of attendance for the 2026-2027 academic year is now approximately $36,000 – $38,000 per year, traditional savings accounts are no longer sufficient.

- Tax Benefits: Contributions grow tax-deferred, and withdrawals are tax-free for qualified education expenses.

- Colorado Advantage: Use CollegeInvest Colorado to access state-specific tax deductions for the 2026 tax year.

- Flexibility: Funds can be used for trade schools, K-12 tuition, and up to $35,000 can be rolled into a Roth IRA (subject to SECURE 2.0 rules).

What are the Benefits of a 529 College Savings Plan for Parents?

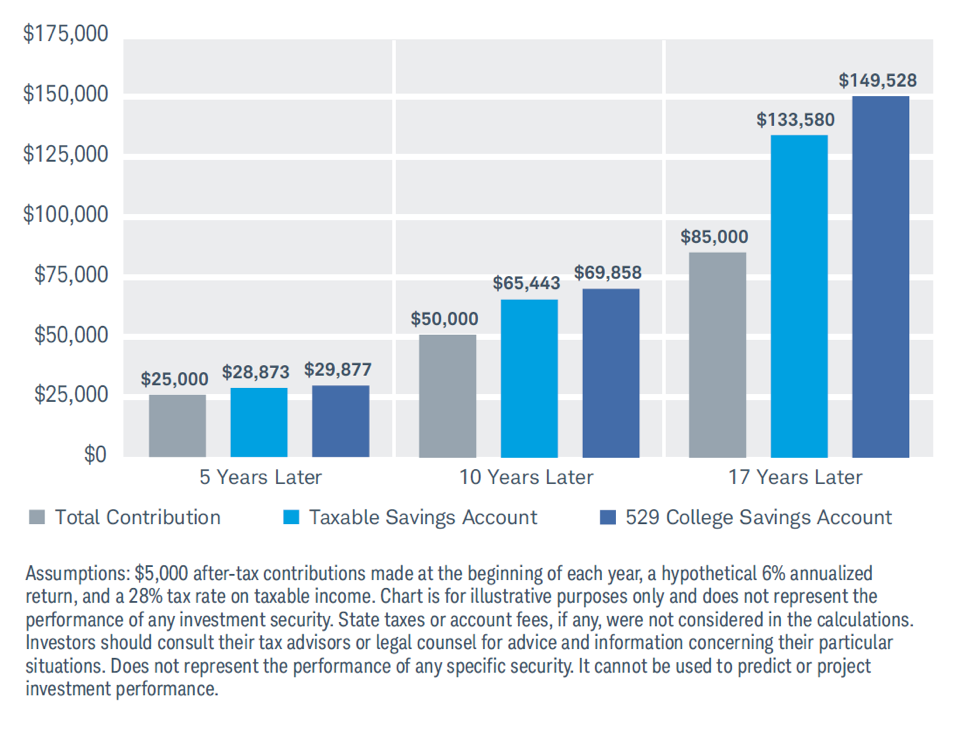

The 529 college savings plan remains the gold standard for education funding. Unlike a standard brokerage account, a 529 allows your investments to grow without being taxed annually. When it comes time to pay for tuition, room, and board, your withdrawals are 100% tax-free.

Colorado’s State-Sponsored Option: CollegeInvest

For local residents, CollegeInvest Colorado offers specific state tax advantages. By choosing a Colorado-sponsored 529 plan, parents can deduct their contributions from their state taxable income, providing an immediate return on investment before the markets even move.

529 Plan Qualified Education Expenses List

One common myth is that 529 funds can only be used for tuition. In 2026, qualified education expenses include:

- Tuition and mandatory fees

- Room and board (for students enrolled at least half-time)

- Books, supplies, and required technology (computers, software, and internet)

- Up to $10,000 per year for K-12 private school tuition

- Registered apprenticeship programs and student loan repayments (up to $10k lifetime)

529 Plan vs. IRA for College: Which is Better in 2026?

While some advisors suggest using a Roth IRA for college, the 529 plan generally offers superior paying for college strategies. 529 plans have significantly higher contribution limits and are specifically shielded from impacting financial aid as heavily as other assets. Furthermore, the 2026 rules continue to allow for the rollover of excess 529 funds into a Roth IRA, mitigating the “over-funding” risk.

How Does a 529 Plan Affect Financial Aid?

A major concern for parents is how a 529 plan affects financial aid eligibility. Because 529 plans owned by parents are considered parental assets, they have a minimal impact on the Student Aid Index (SAI). Usually, only about 5.6% of the asset value is counted, whereas assets owned directly by the student can be counted at 20% or more.

When to Start a 529 Plan for Your Child?

The best when to start a 529 plan is as early as possible. Even small monthly contributions benefit from years of compound growth. If you are planning a move to a better school district or looking to invest in a home near top-tier Colorado universities, your financial roadmap should include both real estate and education savings.

Whether you’re saving for tuition or looking for a home in a specific school district like Boulder or Cherry Creek, Usaj Realty is here to help. Explore our guide on using home equity for college funding or contact us today to find your next home.