The question on every buyer’s mind as we move through 2026 remains the same: when will housing inventory increase? After years of record-low supply and fluctuating interest rates, the “inventory crunch” continues to define the market. To understand the housing supply forecast for 2026, we must look at the specific economic catalysts—from construction costs to local market shifts in the Denver metro area.

How Construction Costs and Lumber Prices Impact the 2026 Housing Market

For years, volatility in lumber prices had a significant impact on the housing market, causing delays and price hikes in new builds. As of early 2026, while supply chains have stabilized, the cost of labor and land remains high.

To solve the housing shortage, developers are increasingly looking toward entry-level home construction incentives. Without a significant increase in new “missing middle” housing, the supply gap will continue to put upward pressure on the prices of existing homes.

The “Rate Lock-In” Effect vs. Historical Mortgage Forbearance

While the industry previously monitored the mortgage forbearance impact on inventory, that era has transitioned into a new challenge: the “Rate Lock-In” effect. Many homeowners who secured 3-4% mortgage rates in previous years are hesitant to sell and trade up into current market rates.

However, as we look at housing shortage solutions for the remainder of 2026, we are seeing a gradual “thawing” as life events—such as relocation or family growth—eventually outweigh the desire to keep a low mortgage rate. This shift is expected to bring more existing homes to the market by late Q3.

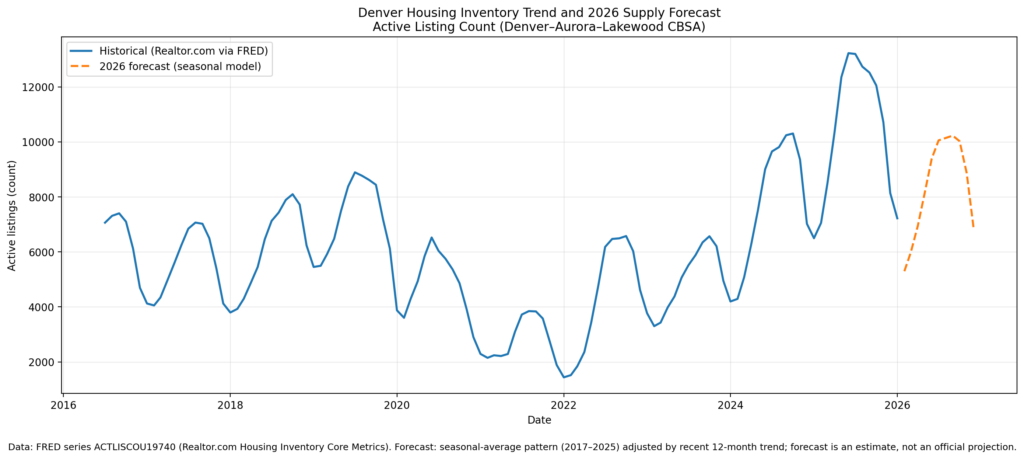

Denver Real Estate Market Trends 2026

The Denver real estate market trends for 2026 show a resilient but tight landscape. While the 2021 median price sat at $595,000, current data for the Denver Metro area shows median home prices hovering between $685,000 and $715,000 depending on the neighborhood.

If you are looking for more affordable options, exploring specific Denver Neighborhoods that are seeing high-density development is key to finding value in this low-inventory environment.

New Construction and Incentives for First-Time Home Buyers in Colorado

One of the most effective ways to increase supply is through targeted policy. We are currently tracking several incentives for first-time home buyers in Colorado designed to offset high entry costs.

If you are a first-time buyer, it is essential to understand the programs available to you. You can learn more about our specialized Buying a Home services to see which tax breaks or down payment assistance programs currently apply to your situation.

Ready to find your next home?

Don’t let low inventory stop you. Explore our resources to stay ahead of the market:

- View Current Denver Listings to see today’s available inventory.

- Schedule a Consultation with a Usaj Realty expert to discuss your 2026 home-buying strategy.

Stay informed on the latest housing shortage solutions and local market shifts by subscribing to our newsletter.