Before diving into the history, check your current purchasing power with our Denver Mortgage Calculator.

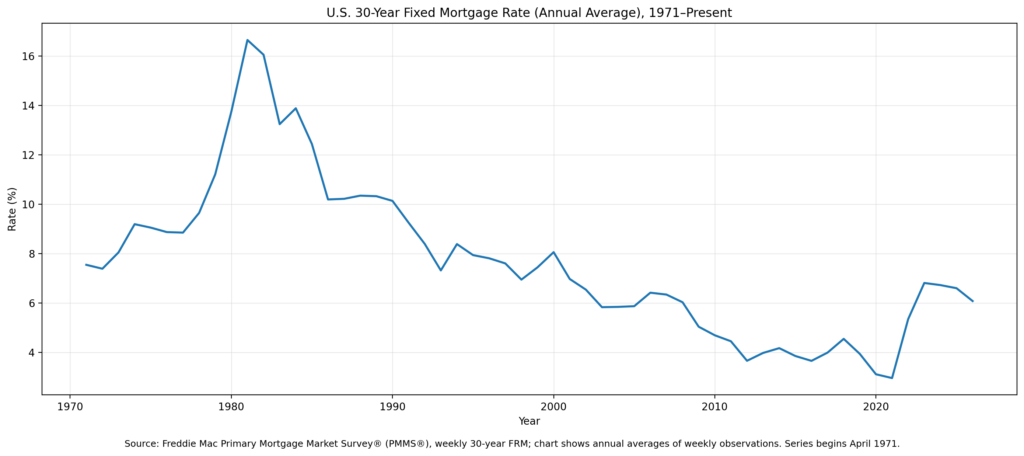

Timeline of 30-Year Fixed Mortgage Interest Rates (1970–2026)

- 1981: All-time highs peaked near 18.6%.

- 1990s: Rates averaged between 7% and 9%.

- 2013: Post-recession lows hit roughly 3.3%.

- 2023-2024: A sharp climb saw rates fluctuating between 7.5% and 8%.

- Early 2026: Current rates have found a “new normal,” stabilizing as inflation cools, providing a more predictable environment for buyers in neighborhoods like LoDo, Highlands, and Cherry Creek.

How Inflation and Denver Real Estate Market Trends Impact Prices

In 2026, the median home price Denver 2026 reflects continued demand in the Rocky Mountain region. While the “sticker price” is higher, real estate remains a premier hedge against inflation. By securing a fixed-rate mortgage now, you lock in your housing costs while future inflation continues to erode the relative value of your debt.

For a detailed breakdown of current neighborhood stats, view our Current Denver Market Report.

Benefits of Homeownership vs Renting: Building Equity in 2026

The Psychology of Home Buying: Is It a Good Time to Buy a House in 2026?

With inventory levels stabilizing in Cherry Creek and the Highlands, 2026 offers a window of opportunity where buyers have more leverage than they did during the bidding wars of years past. If rates drop in the future, you can always refinance; if prices continue to rise, you’ve already captured the equity.

Ready to find your Denver home?

Don’t let the “historical perspective” keep you on the sidelines. Let our expert brokers help you navigate the 2026 market.

Questions about the market? Contact a Usaj Realty Broker today.

Frequently Asked Questions

What is the historical average for a 30-year fixed mortgage rate?

Over the last 50 years, the average interest rate for a 30-year fixed mortgage has hovered around 7.5% to 8%. While the 2-3% rates of 2020-2021 were historic lows, the current rates are actually much more aligned with long-term historical norms.

Are mortgage rates in Denver different from the national average?

While mortgage rates are largely determined by national economic factors and the Federal Reserve, local market conditions in Denver—such as lender competition and local economic health—can influence the specific terms and programs available to Colorado buyers.

Should I wait for mortgage rates to drop before buying a home?

Waiting for rates to drop can be a risky strategy. If rates decrease, buyer demand typically surges, leading to increased competition and higher home prices. Many Denver buyers choose to “marry the house and date the rate,” buying now and planning to refinance if rates drop in the future.

How do interest rates impact my home-buying power?

Higher interest rates increase your monthly mortgage payment, which can reduce the total loan amount you qualify for. It is essential to get pre-approved by a local Denver lender to understand exactly how current rates affect your specific budget and purchasing power.